Financial Education

Why Liquidity Is the First Principle of Sound Financial Architecture

Most financial advice is built around a single objective: grow capital efficiently. Maximize returns on deployed assets. Put every dollar to work. The logic is

Most financial advice is built around a single objective: grow capital efficiently. Maximize returns on deployed assets. Put every dollar to work. The logic is

You have done the thinking. You have looked at the conventional financial advice model; the 401(k)-first, diversify-everything, wait-40-years playbook, and recognized that it was not

Most high earners have done the work on tax strategy. They’ve maximized the 401(k). They’ve evaluated the Roth conversion window. They understand tax-loss harvesting. They’ve

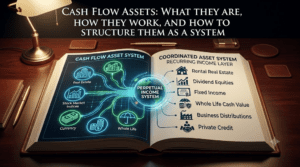

Most articles about cash flow assets give you a list. Real estate. Dividend stocks. Bonds. Maybe a note about REITs. The list is not wrong,

Most financial content is written for people trying to get to a million dollars. Very little is written for people who’ve arrived. Here’s what the

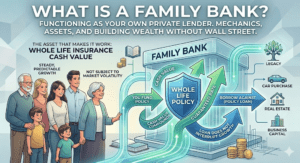

The idea that your family can function like its own private bank isn’t metaphor. Here’s the mechanics, the asset behind it, and how people are

You did the research. You followed the rabbit hole on infinite banking, pushed past the skepticism, built a case for the whole-life policy structure, and

You have spent years building something most people never get close to. The policies are structured. The loans move with intention. The family balance sheet

You’ve built the engine. You understand how infinite banking works, how velocity of money behaves, how a well-structured policy can function as a liquidity lever.

You run opportunity-cost analysis on every capital deployment in your business. Then you look at your personal balance sheet, and that discipline disappears. Not because

If you’ve been searching for “infinite banking” or how to be your own bank, your instinct is pointing at something real. The concept gets one

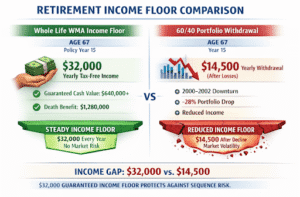

For five decades, defined-benefit pensions were the dominant retirement income vehicle in the United States, not because they were simple, but because they solved a